💹 Bitcoin: Financial Valuation

it seems likely that fiat currencies will remain devalued or even de-anchored, but we may have an alternative from a parallel universe where BTC becomes a treasury reserve

✍️ edit: April 3rd, 2023

Introduction

Greg Foss has 35 years of high yield bond management experience and was once one of the first managers to open high yield bonds in Canada. His friend had appealed to the Canadian Ontario Provincial Court to pass the first BTC spot fund. In finance, high-yield bonds, also known as junk bonds, have different ratings from high to low, from 3A to B. High-yield bonds have a similar history in Canada to Bitcoin, growing from a handful of listed private custodians to being adopted by the Bank of Canada and opened to high-yield bond trading.

BTC is a CDS for multiple currencies

Today, the long-term debt and credit markets are the largest financial assets. But if you compare the credit market to a dog, and equity to a dog's tail, the wind of equity prices can drive credit market shocks, Greg points out, and it would be foolish to ignore the equity valuation of the credit market. In the Latin American debt crisis of the 1980s, the equity book value of Canada's largest bank, RBC, would have evaporated instantly if not for the Brady Plan.

In finance, a Credit Default Swap (CDS) is called a credit default swap and protects its purchaser from credit risk by selling to the defaulter at the Face Value of the bond. If Bitcoin's goal is hard assets and stored value, then Bitcoin's intrinsic value should fluctuate with each country's currency CDS premium negative spreads.

Valuing BTC with Credit Markets

The total global valuation of financial assets should include the credit market, which would then be $900 trillion. Of which the credit market occupies $400 trillion, $300 trillion is real estate, $120 trillion is the equity market, and the remainder is gold, bulk goods, etc. Among them, sovereign debt or national debt occupies a quarter of the credit market, which is $100 trillion.

First, Greg proposes that the valuation of BTC should be calculated like Leverage Enterprise Value. Debt is an important part of the asset structure, and without the valuation of debt, there would be no market value of the credit market. Therefore, although there will be double counting, real estate valuation with leverage should be included in the total global financial asset valuation. Here is the difference between equity and EV analysis and credit analysis. It is clear that it is foolish to ignore the credit market to do equity valuation because credit dominates the entire market. In the event of Tail Risk, the bondholders will be compensated first in liquidation and lastly the equity holders.

Equity valuation: market value = share price x shares issued

Enterprise value: includes DCF model, cash flow analysis, bondholders, EBITDA book analysis

Credit valuation: non-public market debt, default rate, credit score

The U.S. is the leading credit market, with nearly $200 trillion in credit markets. Since the subprime crisis opened the floodgates of quantitative easing in 2008 and the issuance of $10 trillion in federal bonds in 2020 because of the new crown, the size of U.S. federal bonds (excluding municipal or state bonds) is now $30 trillion and the size of unfunded collateralized bonds (including Medicare and Medicaid programs, etc.) is now $162 trillion. By now, you should understand why researchers who ignore the credit market and talk about equity valuation are fools.

To summarize, while BTC has always appeared to the public as a competitor to gold, it is still under-valued at $800 billion compared to the $12 trillion market value of gold and even larger asset classes.

Valuing BTC with Probability

Michael Saylor, founder of Micro Strategy, said, "Energy sellers want to trade their energy for BTC instead of the ever-depreciating petrodollar because BTC indirectly represents the world's energy costs."

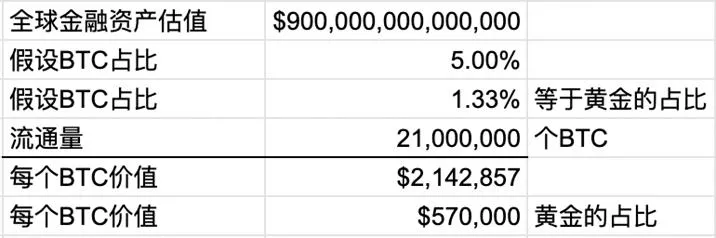

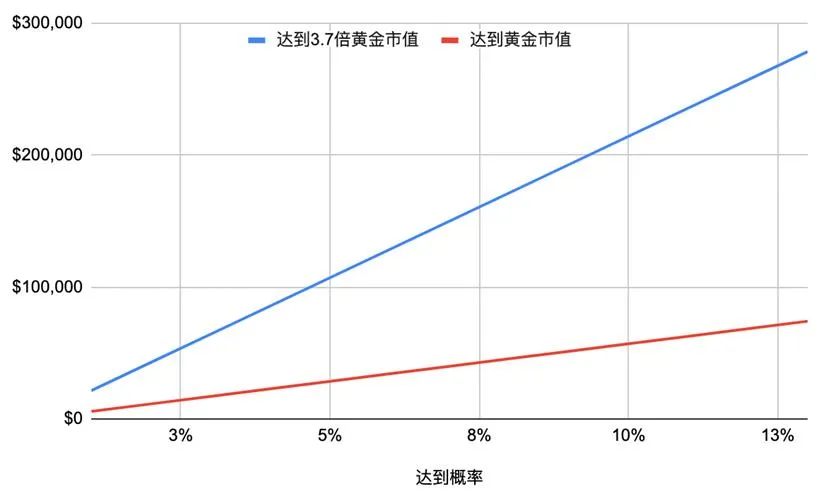

Let's make a simple assumption here, such as assuming that the BTC share is equal to the share of gold in the valuation of global financial assets, or even 3.7 times to 5% of gold. We can multiply the percentage and divide it by the total circulation to get the value of each BTC in the range of $2 million and $500,000, but this is not 100% certain, so we can calculate the expected payoff by the probability of the event.

As you can see, assuming a 10% chance of BTC reaching the gold market cap or 3.7 times the gold market cap, then it should be valued between $57,000 and $214,000 per BTC. At the current valuation of $40,000, one would think that the probability of reaching gold market cap is only 7%, and the probability of reaching 3.7 times gold market cap is only 2%. These are numbers that do not take into account the assumption that hard assets will appreciate in value due to the corresponding future depreciation of the dollar.

And more importantly, unlike the Beta (risk-reward ratio) of BTC in 2017 when it was at $4,000, the current Beta based on the global context and the outbreak of the epidemic has become more sensible. Further, Putin is forcing more countries to flee from petrodollar sanctions after all dollar reserves from energy trading proceeds were all frozen and sanctioned by the U.S. after the start of the U.S.-Russia war. the 30-year history of these sources of dollar devaluation all point to a much higher probability of the future than the current 2% or 7%.

Who is taking the first step?

It is time for practitioners of fixed income bonds or bond discount and premium trading to take the first step. Bonds that are issued when they are yielding 1% will have their face value severely devalued by the 2.9% yielding U.S. bonds currently being sold on the open market. These bonds have been devalued by more than 20% from the face value offered two years ago. Therefore, considering BTC as insurance for these asset portfolios is the best asymmetric and trading opportunity (Asymmetric Trade). According to Greg, this is the best asymmetric trade opportunity he has seen in 35 years that will not liquidate.

Bridgewater hedge fund founder Ray Dalio from 30 years ago when the 10-year U.S. bond yield is still at 14%, began to balance the all-weather risk parity (Risk Parity) allocation to build up his hedge fund. But since the last quarter the stock market and U.S. bonds fell at the same time and in the case of U.S. bond yields have fallen to 1% low, we have seen for the first time in history the U.S. bond yields and NASDAQ at the same time exceeded double-digit percentage swings. Simply put, higher U.S. bond yields and falling U.S. bond pars fell to the same extent as the Nasdaq, meaning that the risk in asset portfolios under Risk Parity was not hedged or balanced so effectively that the performance of assets using these strategies fell out of the expected negative impact. Therefore, there is no longer a more effective traditional asset portfolio to address systemic risk.

Fidelity Investment has published a study on virtual currencies, which points out that there are two categories, one for BTC and another for BTC that does not have the value it represents. According to the data, Fidelity Investment, currently the fourth largest asset management in the world, has allowed its clients and retirement benefit plans (401K) to offer BTC services. In this regard, it seems that other large asset managers that do not provide BTC services will lose a large portion of their client base by not providing BTC services. So, Greg points out that just like the development of high-yield bonds in Canada, it is only a matter of time before BTC becomes a service option for other institutions, and everything will be accelerated whether it is BlackRock or Vanguard Group.

When will the big money come in?

BTC is still under $1 trillion in total market cap, which is too small for big money like Bridgewater or even the $35 trillion in pensions across the US. So for small asset management teams, this time frame is very appropriate, while the big money to enter the risk is very high. So when will these large funds enter? It may not be very realistic to judge the timing of entry, so we might as well do a calculation in terms of probability.

The current U.S. pension funds are basically committed to a 40-year average interest rate of 10% per annum and invest in the traditional allocation ratio of 60% in equity and 40% in bonds. We can assume that in the absence of any risk of global debt default, with 40% invested in bonds and an average coupon rate on bonds at 5%, we can conclude that the return on bonds accounts for 2% of this 10% pension return. Another 2% comes from the fixed income and investments of these pension investors. Greg says that with the current historically high equity valuations and cash flow valuation multiples, it is believed that all pension fund managers are currently burnt out and will either continue to push up the entire stock market with high leverage or find a way to insure the inflated valuations Otherwise, they will continue to wait for the inflated bubble to burst.

Let's imagine a situation where the stock price is 50% off when the systemic risk of default and liquidation comes, the most affected should be the pension fund investors. First, these firefighters, police officers, municipal workers, etc. will find themselves working all their lives to save pensions can not be fulfilled according to the contract or can only pay half of the previous commitment, and then the market volatility as the social instability rises.

Spot ETFs vs. Futures ETFs

The current price of BTC is affected by the historically high futures interest rates and the opening of futures ETFs, which have been artificially compressed like a spring to low prices in the short term. But in the long run, BTC is the only derivative insurance in the world that has the characteristics of shorting debt markets while longing long-term market volatility, and there is no and no perceived need for a long-term long market volatility insurance product in the world. Simply put, the world is convinced that the economy will become more and more stable after the epidemic, and BTC is the only index that opposes this view and can be purchased. Ultimately, those who are bullish that the economy will grow steadily and are shorting BTC will pay for the shorting in the long run.

Greg points out that many hedge funds are using BTC as a Nasdaq fan stock to buy short these overheated sentiments, but they don't realize that it's actually a hedge insurance product that is long on long-term market volatility. No one would argue that the market will always be negatively volatile, but it makes sense to have an extra insurance policy when market volatility is high.

Overall, no matter what the ETF is, legal and regulatory compliance will attract more interested investors, in this case asset managers in the trillions, not just the billions that are currently in the market.

Stock Index Correlation

Many people point out that the price of BTC now has a correlation of up to 0.8 with indices such as the Nasdaq, however historical data is generally for reference only. Moreover, we can see much higher index correlations in the corporate bond trading market because AI trading algorithms are weighting decisions on short-term correlations very heavily. But these algorithms can easily fail due to some artificial manipulation of long-term risk indicators, a specific example being the reduction in interest rates on high-yield bonds being constantly refreshed. BTC is currently more attractive as an investment than it was back in 2016, as the dust has settled on many unknown macro and micro factors.

From a macro perspective, we are almost certain that the fiat currency will keep depreciating 100% of the time. It would have been possible for the U.S. to ride the technology in 2018 and pretty much unwind the 2008 subprime mortgage that led to a death spiral measured in the billions. With the new crown epidemic on the horizon, quantitative easing has begun to create a death spiral measured in trillions. If Americans were wrong to believe that their government would defend the assets they had on hand for 40 years, would they still choose to give their government a chance to believe in the next 40 years or even do a 180-degree turnaround in 2022? The likelihood is extremely slim. On a micro level, the positioning of BTC, including block size decisions and even technology trends, is much clearer than they were several years ago.

Will a rate hike have an impact?

So will a rate hike slow down the devaluation of the dollar or even impact the price of BTC? First, we have figured out that printed fiat money is the root of all evil in this death spiral, so now it becomes a matter of the middle school equality equation. This equation balance needs to be satisfied by the following.

The global economy is not growing fast enough to pay the interest on bonds (economic development < bond interest)

Printing money to support the credit market (slow economic development + unlimited printing of money = interest on bonds)

In summary, the entire credit market has gone haywire. Because no matter how much interest rates are raised, it still won't change the fact that the global economy is slow and needs to keep printing fiat money to pay off the bond interest generated by the sale of bonds. To make matters worse, equity holders are the last ones to receive liquidation compensation when the risk of default comes. Simply put, the current market is not the right place to lend out money, but rather to borrow all the money you can.

Conclusion

Peter Schiff had started with BTC at $10. He could have gotten 40x total assets on the books by putting in 1% of total assets by now, but he never learned from asymmetric trading to reflect on it, instead he kept blocking traditional investors. Although, for now, it seems probable that fiat currencies will keep depreciating or even de-anchoring, we may have a parallel universe option where BTC becomes a treasury reserve and fiat currencies continue to nominally act as a global reserve.